- 31 Oct, 2023

Boosting Your Credit Score with a No Appraisal HELOC: A Win-Win Solution

In need of funds? Get fast Heloc, no appraisal today.

If you’re finding it challenging to get funds even after applying for a HELOC, the issue is probably with the appraisal process. It consumes more time compared to other stages of the application.

A fast HELOC with no appraisal can be a great tool to boost your credit scores as well. In this blog, we will provide you with win-win solutions to get funds quicker and boost your credit score.

Role of credit scores in fast HELOC no appraisal

When was the last time you received a report card? Not the one from school, lol! I am talking about the financial reports that lenders use to assess your creditworthiness.

-

They help in determining your ability to secure mortgages, and lines of credit. Your credit report reflects your total credit score which is used to fix mortgage rates, monthly payments, and lower borrowing costs.

-

Whether you’re looking to improve your credit scores or you already have a desirable score, our blog will help you gain knowledge about the role of credit scores for HELOC.

-

Some individuals will be facing credit challenges, and find it difficult to get the benefits that people with a great credit score experience. So, it is essential to improve the credit score for HELOC, be it with or without an appraisal.

What is HELOC?

Home equity line of credit helps anyone who is in need of funds to meet their financial needs.

It differs from person to person. Some might require funds to consolidate their outstanding debts while others might need the funds to invest in their home improvement projects.

A HELOC helps these individuals borrow money from the equity they have accumulated in their property.

Wondering what equity means? It comprises your home’s value minus the amount you owe in your first mortgage.

The best times to get a HELOC

HELOC could benefit individuals in multiple scenarios, here are some of the best times:

High-interest outstanding debts

HELOC can really serve as a helping hand when you’re completely soaked in high-interest debts. Consider paying it off using a fast HELOC no appraisal option.

Immediate or major household repairs

If your repairs or renovations cost more than thousands of dollars, a HELOC can’t be avoided.

In case of a minor fix, you can either withdraw from the savings account or utilize your tax refunds.

Accumulation of equity in your home

The higher equity you have in your home, the more eligible you become to take out a HELOC.

When there’s more equity, you have the freedom to withdraw money for various purposes. This is not possible when there’s limited equity.

It is highly applicable when you have seen an increase in the price of your home in recent times.

Appraisal dilemma

Traditional appraisal offers the most accurate value of the property and helps the homeowners get better loan amounts.

While lenders assess the current value of your home to determine the available equity, it takes a lot of time to receive the funds.

Appraisals can be usually expensive, depending on the location and complexity of the appraisal process. This adds up to the overall cost of obtaining the HELOC.

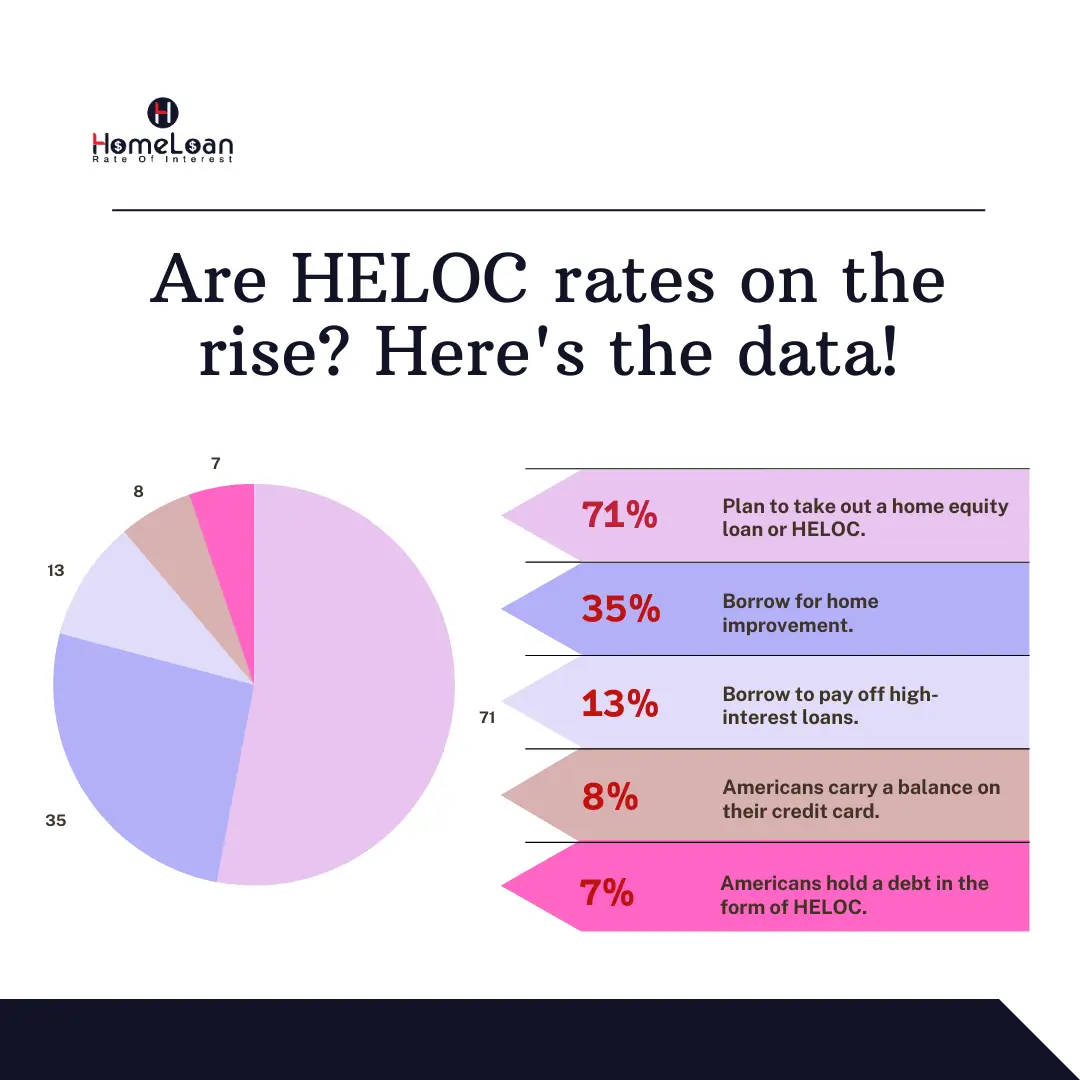

Why do people go for a no-appraisal HELOC?

Many homeowners of today see a no-appraisal HELOC as an attractive option. Here’s a breakdown of several reasons why people go for a no-appraisal HELOC.

Save time and money

A fast HELOC no appraisal option can help homeowners save a lot of time and minimize their appraisal expenses. They can get their funds without much delay.

Faster approval

Skipping the traditional appraisal process will help lenders approve the loan faster and homeowners can later use the funds for immediate home improvements and debt consolidation.

Focused on credit score

Some no-appraisal HELOCs offer the loan amount based on the creditworthiness of the homeowner.

This makes it a preferred option for individuals with strong financial profiles or individuals who are aiming to up their credit score.

How can no-appraisal HELOC boost your credit score?

It is a universal fact that a higher credit score for HELOC can help homeowners qualify for favorable loan terms with lower interest rates. But, what if your credit score is not up to the mark?

There’s a way to increase it! Applying for a fast HELOC no appraisal can be a valuable tool to improve your credit score when used responsibly. Here’s how:

Credit utilization rate

-

Credit scoring models interpret lower credit utilization rates as a good indicator of managing credit payments.

-

It highlights that an individual with a lower credit utilization ratio is using less available credit.

-

The ratio represents the amount of revolving credit currently used by the borrower compared to the total number of available credit limits.

-

So, if you’re being responsible by using your no-appraisal HELOC to pay off higher-interest debt, you can reduce your credit utilization ratio.

-

Remember, if you take out huge sums of money to consolidate your debts, your credit utilization will go up and this can impact your credit score for HELOC.

-

-

Making timely payments

-

If you’re aiming for a great credit score, consider making on-time payments on your no-appraisal HELOC.

-

Your payment history has a huge influence on your credit score and if you want to boost it, develop a plan and manage all your credit payments along with other day-to-day expenses.

-

This ultimately demonstrates responsible financial behavior and contributes to leveraging a strong payment history.

-

-

A mix of credit types

-

Having a diverse credit portfolio will have a positive impact on your credit score for HELOC. Credit scoring models take into consideration a mix of credit types such as installment loans, and revolving credit.

-

A fast HELOC no appraisal is a part of revolving credit and can enhance your credit score as it demonstrates your ability to responsibly manage different credit types.

-

Finding the no-appraisal HELOC lenders

Do you want a lender who not only offers no-appraisal HELOCs but also aligns with your financial goals and values? You have come to the right place, we help homeowners go through a simplified HELOC process.

In order to have a successful borrowing experience, selecting the right lender is crucial, let us help you do it right.

Credibility and reputation

-

Look for lenders who have had a higher success rate in processing no-appraisal HELOC applications. Choose a lender who has a solid reputation and satisfied customer reviews.

-

Understand if the lender has a history of following trustworthy lending practices and credible endorsements.

-

Transparent terms and conditions

-

Go for a lender who is transparent and open about communicating their terms and conditions to the borrowers.

-

Check if they’re ready to provide dedicated assistance to explain their terms, interest rates, fees, and repayment policies associated with the No Appraisal HELOC.

-

Accessibility and support

-

A lender who has responsive customer support can make your borrowing experience much smoother. Understand if they will be available to provide prompt assistance to your queries.

-

Competitive rates

-

You need to be good at comparing interest rates from multiple lenders to get the best deals. Some lenders will provide the best interest rate if you show them a great credit record.

-

While a no-appraisal HELOC is a favorable option by itself, it is still important to shop around for the best rates.

-

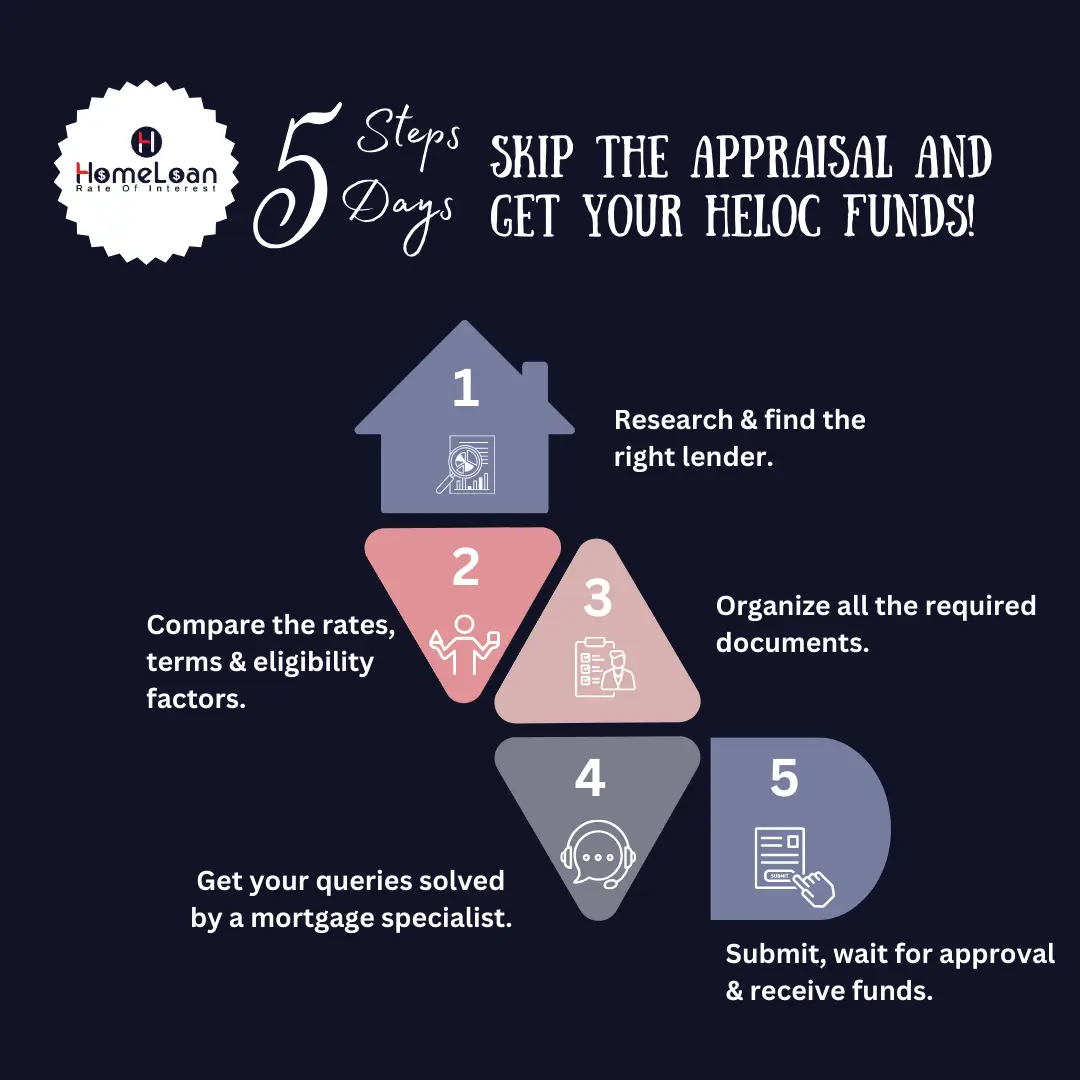

The application process for no-appraisal HELOC

It’s time for us to plunge into the step-by-step process of applying for a no-appraisal HELOC. It is straightforward and pretty simple compared to a traditional HELOC.

Research and shop around

-

Different lenders will have different offerings. It is the responsibility of a borrower to surf the internet and check the interest rates, eligibility requirements, and terms offered by each lender to make a well-informed decision.

-

Gather all the documents required

-

For a no-appraisal HELOC, lenders usually request specific documentation for your application. Some of these documents include -

Proof of income & asset documentation.

Tax returns.

Mortgage payment statements.

Property documents.

Personal government proof IDs.

-

This might vary depending on your financial situation, and some lenders require additional documentation as well. Check with your lenders for accurate information.

-

Consult with a mortgage specialist

-

Many lending institutions offer you a dedicated specialist who will be there to assist you throughout your application process. Make sure to get your queries answered by these specialists before moving ahead with your application.

-

They will be able to assist you throughout the application process and ensure you submit a perfect application.

-

Submit and wait for approval

-

Once you have decided on the amount you want to borrow, go ahead and submit the application. Maintain accuracy in order to avoid delays.

-

As the appraisal process has been skipped, the approval process will speed up and you shall wait until your approval.

-

Receive your funds

-

Once approved, you will receive the funds you have been waiting for days. Remember to not overuse the funds just because it’s available.

-

It will affect your credit utilization ratio and ultimately your credit score as well.

-

Budget your no-appraisal HELOC funds strategically in order to maintain a lower credit utilization ratio.

To boost your credit score for HELOC, you need to monitor your credit spending, regularly review your financial statements, and make adjustments whenever needed.

As timely payments reflect your credit score, try setting up automatic payments in order to avoid missed or late payments.

On the whole, a fast HELOC no appraisal is a game-changing financial solution that offers a perfect balance of accessibility and speed in receiving funds and raising your credit score.